FRAUD REMINDER: WeStreet will never call, text, or email you to ask for personal details, verification codes, or account information. Even if the message appears to be from us, do not share your information. If someone attempts to contact you on behalf of WeStreet asking for sensitive information please report the suspicious activity to our Care Center at 918-610-0200.

Es Donde Perteneces

Descubre la Iniciativa Hispana de WeStreet: un espacio creado especialmente para ti. Nuestra página en español ofrece educación financiera y detalles sobre nuestros productos y servicios.

Discover WeStreet in Spanish: a space created especially for you. Our website in Spanish offers financial education and details about our products and services.

You’re in the middle of paying your water bill online when all of a sudden they ask for your checking account routing number. In a panic, you close the browser window. Is it time to start digging through your junk drawer looking for your checkbook? Which one is the checking account routing number anyway? And why in the world would they need that information?

Where Is My Routing Number?

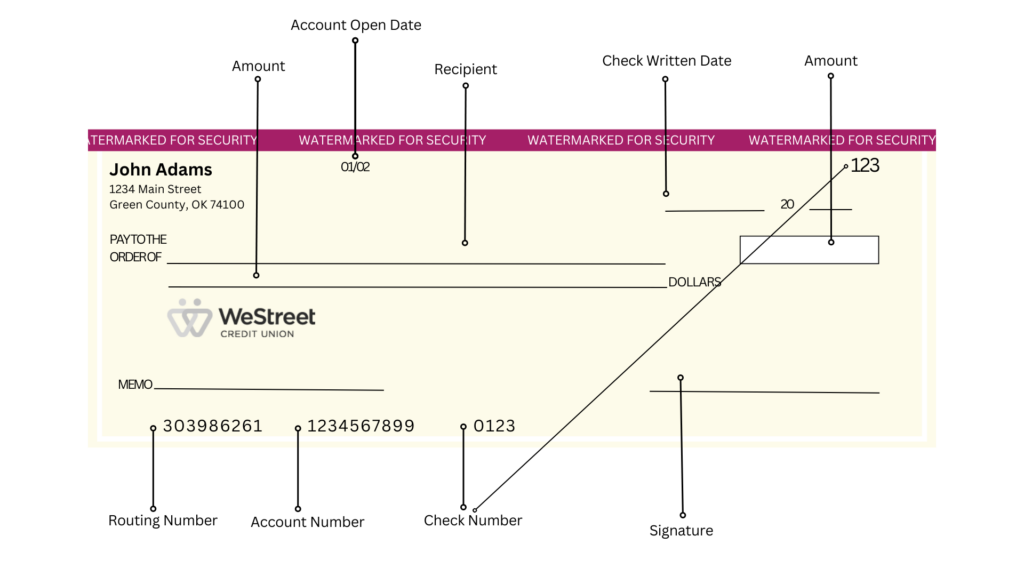

Your routing number is usually located on the bottom-left corner of your checks. Look for a nine-digit number. Routing numbers are specific to a financial institution.

You can also find any routing number quickly by typing “[Your Financial Institution’s Name] routing number” into your favorite search engine. Most banks and credit unions list their routing number online for just such occasions. You can also ask Google Assistant or Alexa if you have voice services.

What Is A Routing Number?

This set of numbers is a unique identification code assigned to that identifies the financial institution. This code is used for electronic transactions such as a funds transfer, direct deposit, digital checks and bill payments. It is often referred to as routing number, aba routing number, or routing transit number.

What About My Account Number?

Don’t confuse your routing number with your account number, which is also located in the bottom-left corner of your checks. The bank account number is usually listed immediately after the routing number. You will have a different number for each of your accounts including any checking accounts, or savings accounts.

For most transactions, you will need both your routing and account numbers to set up an ACH payment, connect a deposit account for a service like PayPal or Venmo, or set up direct deposit.

If you don’t have any physical checks around, you can usually find your account number by logging in to Online Banking and viewing your accounts. Learn more about locating your account and routing number online here.

What’s The Memo Line For?

The memo line is just a place for you to put a note about the purpose of the check you’re writing. If it’s a rent check, write “rent” to remind you when you see a scan of the check in your online banking statement later.

Or, if you’re old school, the memo will go on your carbon copy to be used when you balance your checkbook at the end of the month. But, if you’re still doing that, you should consider signing up for Online Banking.

Who Do I Pay To The Order of?

This line is where you would write the recipient’s name or the name of the company you are paying. It’s a good idea to check spelling or whether the person you are writing a check to operates under the name of a small business or other entity.

“Who should I make this out to?” is a good question to ask before you put pen to watermarked paper. Banks may not accept checks with incorrect spelling or names because it doesn’t match what is in their system.

Spell It Out In Dollars & Cents

Perhaps the most grammatically confusing part of writing a check is spelling out the amount that you’re writing the check for. It’s easy enough to write $150.67 in the Amount box, but it quickly becomes and internal debate between “One Hundred Fifty and 67/100” or “One Hundred AND Fifty and 67/100″ (hint: the first one is correct).

Just know that the bank is less concerned with your grammar in this section and more concerned with ensuring that the number you wrote in the amount box matches what you spell on the line. That way, the recipient can’t get away with adding an extra zero to the amount box.

Where Do I Sign?

The last thing you should do once you’ve filled out your check is to sign on the line in the lower-right corner. This proves your check is legitimate and the bank can compare your signature to past signatures on file to ensure that you actually wrote the check. Believe it or not, people sometimes try to fake checks.

I Endorse This Message

If you’re the recipient of the check, you may need to endorse it on the back by signing on the faint line near the top of the check when it’s held vertically.

If you’re performing a mobile deposit, your bank or credit union may also require you to indicate that the check is intended for mobile deposit on the back of the check.

This article is for educational purposes only. WeStreet FCU makes no representations as to the accuracy, completeness, or specific suitability of any information presented. Information provided should not be relied on or interpreted as legal, tax or financial advice. Nor does the information directly relate to our products and/or services terms and conditions.